Inflation

There are certainly a lot of headwinds in the market with both inflation and interest rates climbing. As we are all painfully aware, the U.S. inflation rate is currently the highest it has been in 40 years. While there was hope that the inflation rate would ease as the year progressed (8.5% in March), that has not happened. (See the chart below).But it could/should. Why? Because the inflation rate that is disseminated by the government is a comparison of prices to the prior year. 2020 was an historically low year for inflation because demand plummeted due to the pandemic. In 2021 inflation started to tick up as things started to open up post vaccinations, etc.. We may not be printing more forty-year highs because 2022 Q2 – Q4 prices will be compared to prices for the same time period in 2021. However, that does not mean that the high cost of goods and services will subside.

Inflation Rates 2020 – 2022

So, inflation numbers may not stay at these 40-year highs, but that doesn’t mean things will cost less. It just means that the comparison to last year is not as extreme as the 2021 and Q1 2022 comparisons were. The month-to-month comparison of inflation rates, as opposed to year-to- year comparison, is still very concerning. Monthly inflation has continued at high rates over the last year. March of this year had the highest monthly inflation rate over the last year plus. (Most likely due to the war in Ukraine).

We all know that inflation has been a problem for well over a year now and is a many-faceted problem.With higher energy prices, supply chain issues, higher labor costs, etc. inflation may remain elevated for a while. These issues will need to be addressed and demand has to wane.

Government intervention is another contributing factor to the current high interest rates. The Congress and executive’s branch’s largess of stimulus money to individuals and businesses as well as numerous “infrastructure”*** bills have flooded the markets with money. Money in people’s hands obviously translates into demand which exacerbates the inflation problem.

With the lack of adults in the room in Washington (on both sides of the aisle) to address the problem, the inflation problem may continue. Larry Summers is one of many economists that have been strenuously voicing their concerns, but the ‘supposed’ adults in charge appear not to be listening.

On top of Congress and the executive branch’s largess, the Federal Reserve has showered the markets with unending goodies over the last decade. These accommodative policies, on top of the stimulus money and “infrastructure” spending created fertile ground for inflation. These policies continue to fertilize that fertile inflation ground. We are paying the price for the Federal Reserve’s multi-year accommodative policies of low interest rates, bond buying and other shenanigans. They are way out over their skis and acting outside of their mandate.

The Federal Reserve raising interest rates a quarter point at a time, as they recently did, is not going to reduce the insatiable demand. Consumers, businesses, and the government competing for goods (with “infrastructure” bills) results in plenty of cash to spend and continued high demand for goods and services.

*** I have written about positive infrastructure spending multiple times. Think of the highway system and many other examples where the government (us collectively) spent the money and received it back in tax dollars later. This is best done when the economy is down to prime the economic pump, not when we have high inflation when the government will be chasing the same scarce goods, insanity!

Interest Rates

This is simple, interest rates are rising. They have to rise to tame inflation. If the Federal Reserve doesn’t aggressively raise interest rates, we will all lose more and more of our paychecks to inflation. Inflation is the most insidious tax of all, especially for those with lower and middle incomes.

Markets

The Federal Reserve’s (Fed) accommodative policies make the market go up.

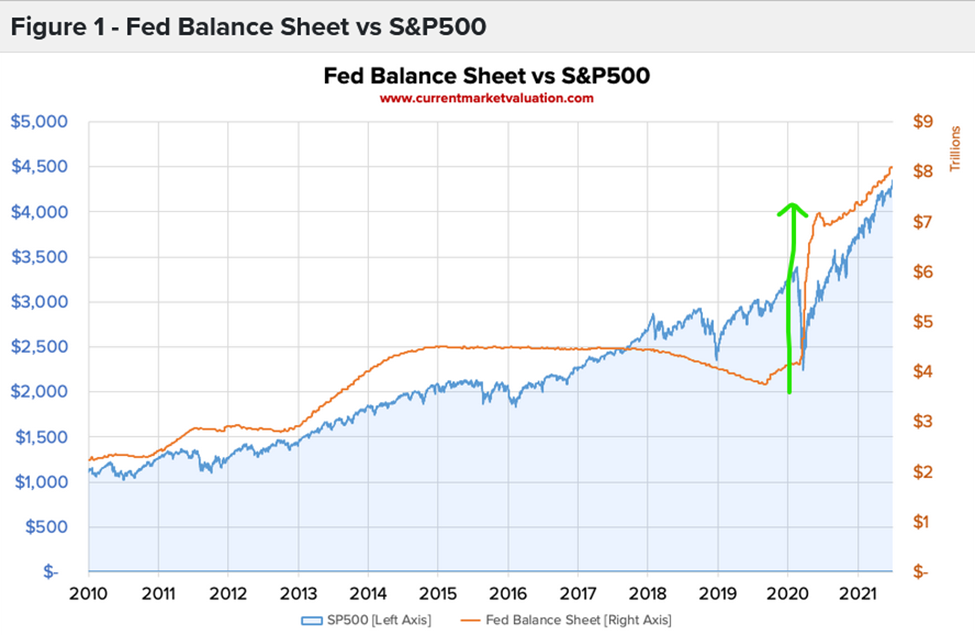

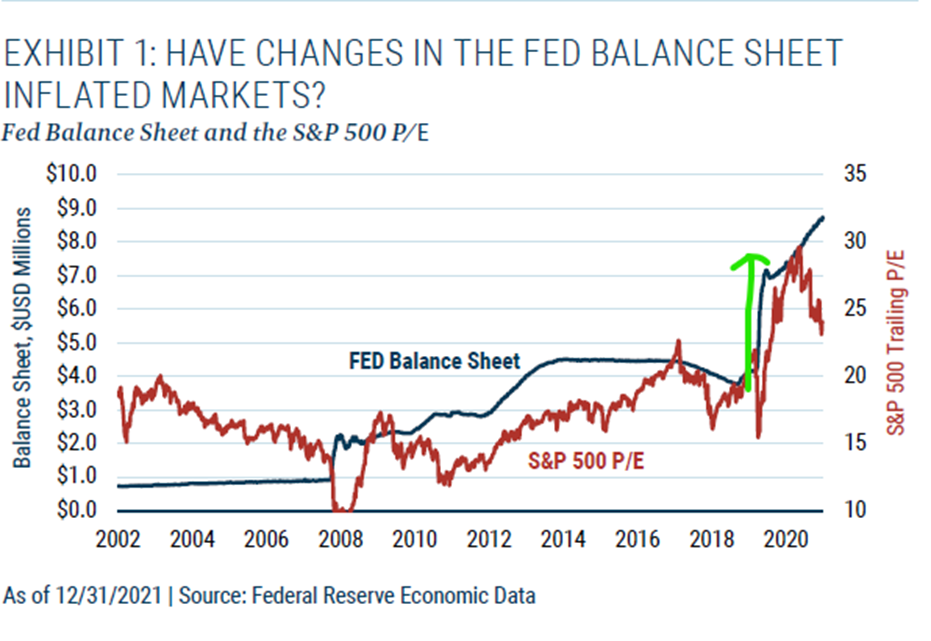

The first chart below shows the value of the S&P 500 in comparison to the Fed’s balance sheet (e.g. what the Fed owns in bonds, etc. that they have purchased to stimulate the economy). The second shows the Price/Earnings ratio of the S&P 500 in comparison to the Fed’s balance sheet. Both graphs clearly show that as the Fed increases its balance sheet (accommodative policies), the stock market grows.

Source – Currentmarketvaluation.com

Source – GMO’s article – Watch-out-for-the-Balance-sheet

Now The Federal Reserve is talking about raising rates and reducing their balance sheet. Look out below! We will see if they follow through. The Fed’s mandate is not to manipulate markets, but it is obvious that they feel it is.

At some point, the fear of inflation and the Fed’s reaction may push the market down regardless of how aggressive the Fed is. The market is always looking to the future.

Investing in this Environment

If you are a buy-and-hold investor, make sure that you have reviewed your risk and how much you will lose in the average bear market. We explain this in our Market Value Update blog post. In the average bear market, the stock market loses over 50% of its value. Therefore, if you have 60% invested in stocks, expect at least a 30% loss to your overall portfolio. (The math, multiply the stock allocation of your portfolio x 50% for a reality check.). The problem in this environment is that bonds are also very overvalued and will not provide the buffer to stocks that they generally do. Take that into consideration when you are calculating expected losses in a bear market.

The key is knowing how much you can expect to lose so you don’t freak out and sell when the market is down. You need to make your decision now as to how much you can afford and are emotionally willing to lose. The further away you are from needing the money, the more comfortable you can be with letting it ride. When you are getting closer to your goal/closer to needing the money is when it becomes Important to Avoid Large Losses.

Investing – How We Do It

At Bartley Financial we take a more active two-pronged approach to investing. First, valuation, which is a long-term view, and second, momentum of both the entire market and, as importantly, the industries and sectors that are performing the best. This can add significant diversification and gains to your portfolio.

The markets can be overvalued, even extremely overvalued, for years. If you base your investment approach only on valuation, then you will miss out on many good years in the market. That is why we also also consider market momentum in our investment approach.

Bottom line, we are opportunistic investors.

At Bartley Financial, we only believe in a completely passive buy-and-hold approach to investing when; the market is at a good or reasonable value OR you have ample time (decades!) before you need the money, and you lack the time and experience to use momentum in your investment allocation decisions.

At Bartley Financial we would love to assist you with not only your investment decisions but also your broader financial planning decisions. Whether you are an individual investor or a business owner concerned with maintaining or building on your successes or planning for succession of the business, we can help you. From our years of experience (growing up in a small business, as CPA’s etc.), we shine in all of these areas. We Live to Plan so you can Plan to Live!

Thanks for your time and interest.